While soon-to-be graduates prepare for the next step and their summer freedoms, another conversation emerges, not about weekend plans and exams, but about wallets and their contents.

Having a credit card represents a major milestone when attending college or starting a job soon.

However, credit card use is not a game to be played lightly, especially by inexperienced students.

There are two types of cards: heavyweights and starters. While the former may offer luxurious perks, it is crucial to know when a card becomes an instrument of extortion.

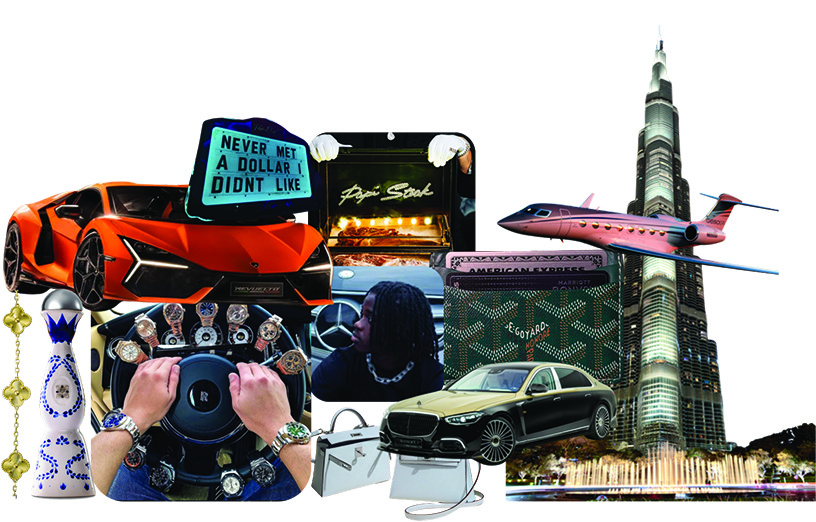

Have you ever noticed a student traveling across the globe and posting pictures in their Tiktok account as if everything was “free”?

First, there’s the “secret” weapon of the credit-card community, the Ritz-Carlton™ Credit Card by Chase.

Not available online, the card comes with an impressive price tag: $450 per year and a lot of great features.

Cardholders can expect annual rewards of up to 85,000 Marriott Bonvoy points, automatic Gold Elite status, and $300 in travel credits, as mentioned in The Points Guy’s review.

It is the card to make your Ritz-Carlton dreams come true after you have graduated.

Secondly, the American Express Platinum Card® stands out as the “It Card” of 2026, despite its astronomical $895 annual fee.

What makes this card so appealing is that it offers $3,500 in annual credits, including $200 in Uber Cash and $400 in dining credits. Moreover, holders of this card can enjoy VIP access to over 1,555 airport lounges, leagues more than the competition.

Junior Blake Cohen says that “if the annual fee is a no-brainer, then the annual rewards make sense,” but if you don’t have the money, “all the perks could start to look like a trap, dropping consumers into situations where they’re spending more money; inevitably leading them down the path of poor financial habits.”

While comparing these premium cards is fun, both Ritz and Platinum are either out of reach or a poor first choice for most students.

Those entering their freshman year of college or earning their first paycheck should look into some starter cards.

There is an impressive list of credit cards for students, including the popular Discover it® Student Cash Back, which provides 5% cash back on rotating categories like gas stations and restaurants, with a $0 annual fee.

It might make sense to go with the Capital One Quicksilver Student Cash Rewards Credit Card, with its 1.5% cash back on all purchases.

These cards were made to give new members a chance to prove to that they can responsibly handle a credit card.

Personal Finance teacher Grant Macnaughton has avoided credit cards throughout his life. “I don’t want to yell down from the high tower, but I’ve seen debt run rampant amongst friend groups. A $1,000 of debt to a credit card will have compound interest working against you. Paying only minimums on the debt will leave you with payments for years and a total amount paid of over $2,600.” (Assuming the average interest rate found on typical cards)

That’s over two and a half times the amount of money you initially owed.

All to prove that a credit card should always be thought of as a debit card, and paid off in full at the end of every month.

The truth is that credit cards do not exist to give away free money. A card like the Amex Platinum is excellent for those who can afford it.

A student credit card, such as Quicksilver®, is an outstanding teacher for those still learning to manage finances.

The ultimate “battle” is not between Ritz-Carlton and Amex; it’s aspiring users & students against the interest rate.

Students need to understand that cards are not free money machines and that they have a dark side when used improperly.